When it comes to managing personal finances, understanding your monthly payments is crucial. Many homeowners and borrowers find themselves grappling with the complexities of their mortgage or loan payments. Among the various components of these payments, the monthly principal and interest payment stands out as a significant figure that holds the key to financial planning. If your monthly principal and interest payment is $3,078.59, you may wonder what the total amount represents in the grand scheme of your financial commitment.

In this article, we will delve into the implications of a monthly principal and interest payment of $3,078.59. We'll explore how this figure impacts your overall financial situation, including the total cost of your loan over its lifespan. Whether you’re a first-time homebuyer or looking to refinance, understanding this aspect of your finances can help you make informed decisions.

Let’s break down the intricacies of this monthly payment. By examining the components that make up your payment and calculating the total cost, you’ll gain insights into budgeting and long-term financial planning. So, what does a monthly principal and interest payment of $3,078.59 truly signify? Let’s find out!

What is Included in the Monthly Principal and Interest Payment?

Your monthly principal and interest payment is a critical part of repaying your mortgage or loan. But what exactly does it include? Here’s a breakdown:

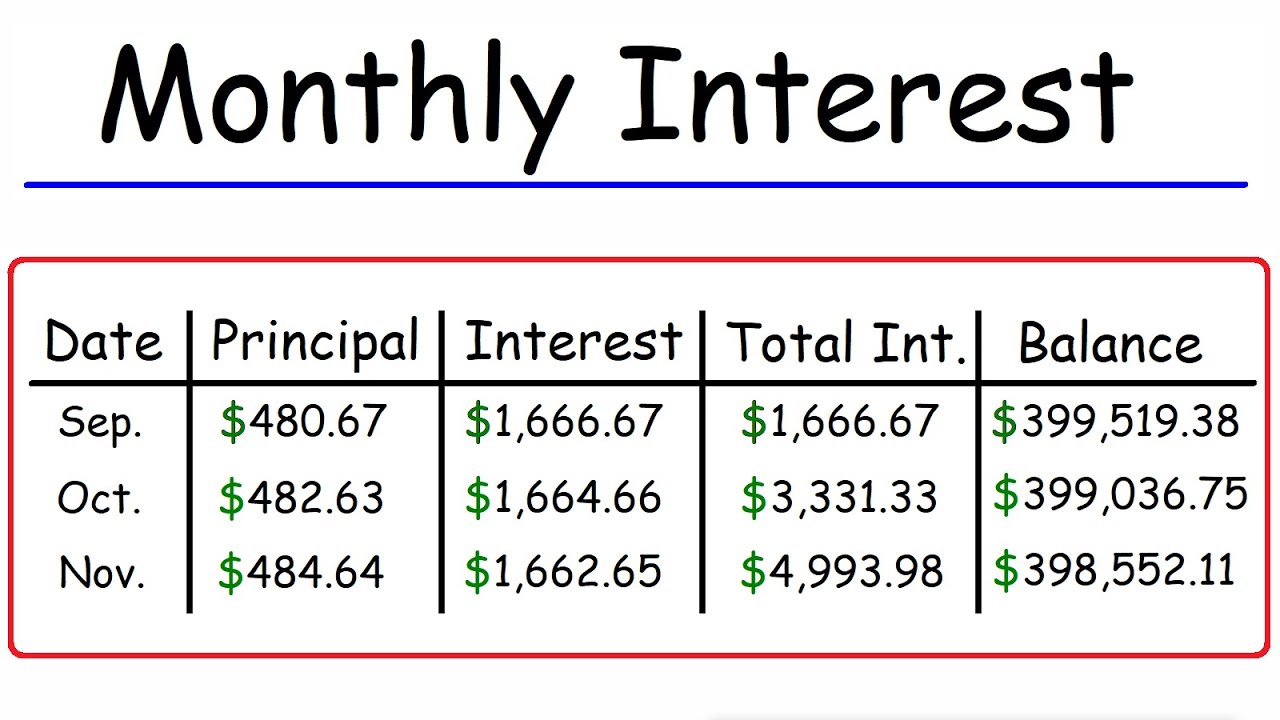

- Principal: This is the amount you borrowed and are required to repay.

- Interest: This is the cost of borrowing money, calculated as a percentage of the principal.

Understanding these two components is essential for grasping the total commitment of your loan.

How Do You Calculate the Total Cost of Your Loan?

Calculating the total cost of your loan involves more than just knowing your monthly payment. To determine the overall cost, you need to consider the loan term and interest rate. Here’s a simple formula:

- Total Cost = Monthly Payment x Number of Payments

If your monthly principal and interest payment is $3,078.59 and your loan term is 30 years (360 months), the calculation would look like this:

- Total Cost = $3,078.59 x 360 = $1,109,485.40

What Factors Influence Your Monthly Payment?

Several factors can influence the amount of your monthly principal and interest payment:

- Loan Amount: A larger loan amount will result in higher monthly payments.

- Interest Rate: A higher interest rate increases your payment.

- Loan Term: Shorter loan terms mean higher monthly payments but less interest paid over time.

How Does a $3,078.59 Payment Compare to Average Payments?

To put your monthly principal and interest payment of $3,078.59 into perspective, let's compare it to average mortgage payments in your area. Depending on your location, the average payment can vary significantly. For instance, in some urban areas, payments may exceed this amount due to higher real estate prices.

What is the Impact of Extra Payments on Your Loan?

Making extra payments towards your principal can significantly reduce the total cost of your loan. Here’s how:

- Reduces Interest: By decreasing the principal balance, you pay less in interest over time.

- Shortens Loan Term: Extra payments can help you pay off your loan faster.

What Happens if You Miss a Payment?

Missing a monthly principal and interest payment of $3,078.59 can have serious repercussions:

- Late Fees: Most lenders charge a fee for late payments.

- Impact on Credit Score: Late payments can negatively affect your credit score.

- Foreclosure Risk: Continued missed payments can lead to foreclosure.

How Can You Manage Your Monthly Payments Effectively?

Managing your monthly payment effectively is essential to maintaining financial stability. Here are some strategies:

- Budgeting: Create a budget that accommodates your monthly payment.

- Automate Payments: Set up automatic payments to avoid late fees.

- Refinancing: Consider refinancing options for a better interest rate.

What Resources Are Available for Homeowners?

There are numerous resources available to assist homeowners in understanding and managing their monthly payments:

- Financial Advisors: Consult with a financial expert for personalized advice.

- Online Calculators: Use online tools to estimate payments and total costs.

- Homebuyer Workshops: Attend workshops to learn about mortgages and budgeting.

What Should You Do If You Can't Afford Your Monthly Payment?

If you find yourself struggling to afford your monthly principal and interest payment of $3,078.59, consider the following options:

- Contact Your Lender: Discuss your situation and explore options for temporary relief.

- Seek Counseling: Look for housing counseling services for assistance.

- Explore Government Programs: Research programs designed to help homeowners in financial distress.

Conclusion: Understanding Your Financial Commitment

In conclusion, if your monthly principal and interest payment is $3,078.59, it's crucial to understand what this figure represents in terms of total loan cost and financial responsibility. By breaking down the components of your payment, calculating the total cost, and exploring options for managing your payment effectively, you can take control of your financial future. Remember, understanding your finances is a key step toward achieving your financial goals.

You Might Also Like

Empowering National Governments: Strategies That Could Make Them Less Dependent On VassalsUnveiling The Enigma Of Shy_Dy: A Journey Through Art And Expression

Understanding The Recent Ramen Noodles Recall By The FDA

Unlocking The Sweet Secrets: A Comprehensive Review Of Black Thai Honey

Unveiling The Truth: Is Eilish Holton Married?

Article Recommendations

![[Solved] Determine the monthly principal and interest payment for a 15 year... Course Hero](https://i2.wp.com/www.coursehero.com/qa/attachment/32727467/)