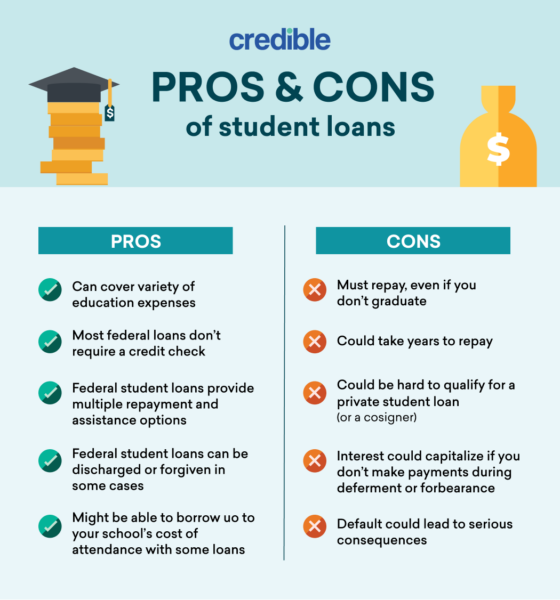

When it comes to financing higher education, many students and families find themselves navigating a complex landscape of loan options. Federal loans can offer lower interest rates and more favorable repayment terms compared to private loans, making them an attractive choice for millions. However, one critical aspect that often goes overlooked is the potential downside of borrowing the maximum allowed amount of federal loans. This article aims to shed light on this issue, exploring not just the implications of such borrowing but also the broader financial landscape that students must consider.

One of the most significant concerns surrounding the decision to borrow the maximum allowed amount is the long-term financial burden that can ensue. While it may seem appealing to cover all educational costs upfront, the reality of student debt can lead to overwhelming monthly payments that can take years, if not decades, to pay off. This financial strain can affect other areas of life, such as the ability to purchase a home, invest in retirement, or even pursue further education. Understanding these implications is crucial for anyone considering the maximum borrowing option.

Additionally, the psychological impact of carrying a substantial amount of debt can’t be ignored. The pressure and anxiety associated with student loans can be immense, often affecting mental health and overall well-being. It is vital for borrowers to weigh these emotional factors alongside the financial considerations when deciding how much to borrow. In this article, we will explore the various dimensions of this topic, answering essential questions and providing insights into the ramifications of borrowing the maximum allowed amount of federal loans.

What is the Maximum Allowed Amount for Federal Loans?

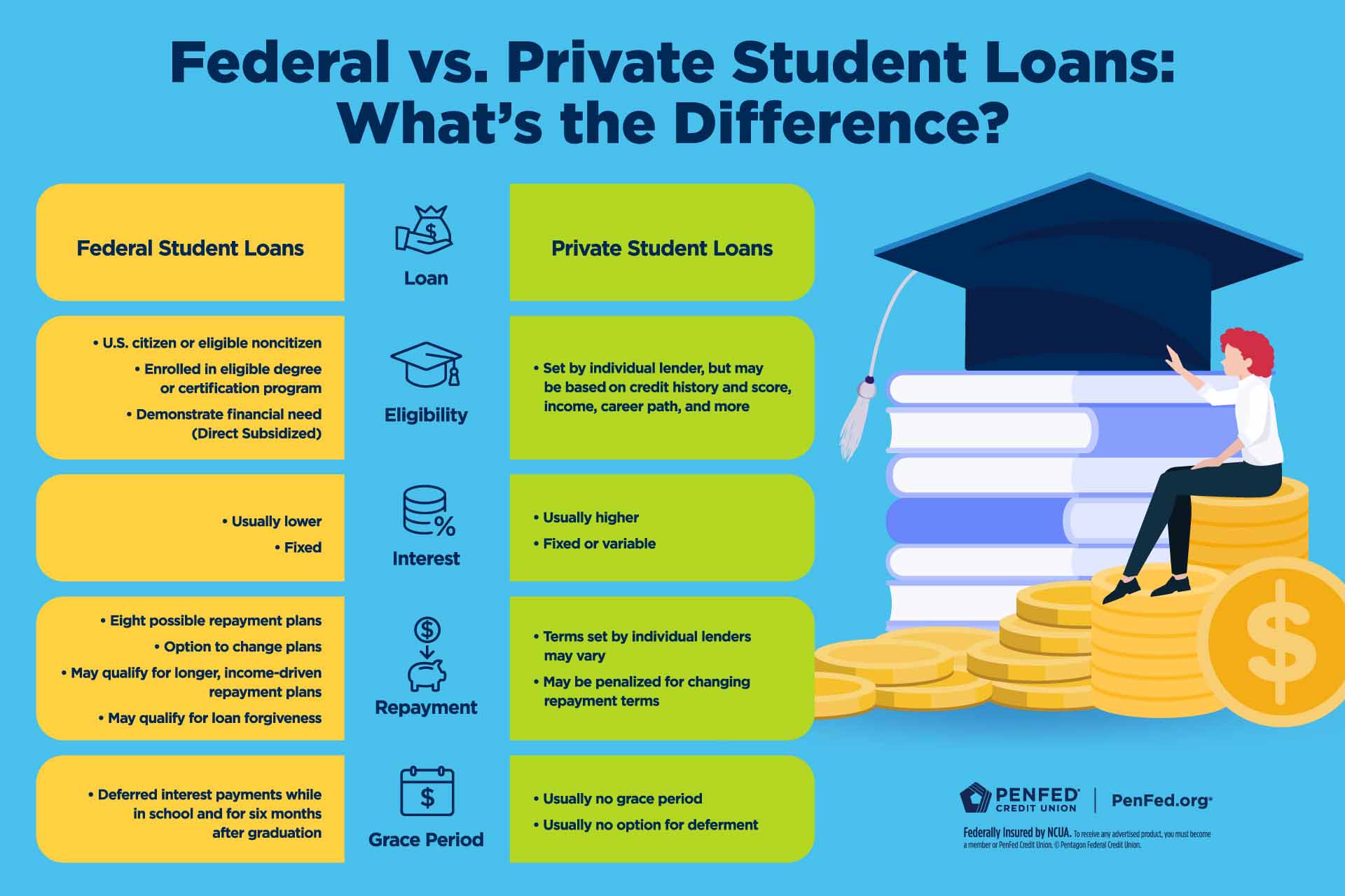

The federal loan programs, such as Direct Subsidized and Unsubsidized Loans, set specific borrowing limits based on a student's year in school and dependency status. Understanding these limits is essential for students and families as they navigate their financing options. For instance, undergraduate students can borrow different amounts annually, which cap at certain totals over the course of their education. Knowing these figures can help in planning how much to borrow responsibly.

How Do Federal Loan Limits Vary by Student Type?

Federal loan limits differ for dependent and independent students. Dependent students typically have lower borrowing limits compared to independent students, who may qualify for higher amounts due to their financial situations. This distinction is crucial when considering the total amount of debt one might accumulate. Here is a breakdown of the annual borrowing limits:

- Dependent Undergraduates: $5,500 to $7,500

- Independent Undergraduates: $9,500 to $12,500

- Graduate Students: Up to $20,500

What Are the Implications of Borrowing the Maximum Amount?

Choosing to borrow the maximum amount can lead to significant challenges down the road. One of the most immediate implications is the risk of overborrowing, which can result in higher monthly payments and increased interest costs over time. When students take out more loans than they need, they may find themselves paying for unnecessary expenses, which can exacerbate their financial situation post-graduation.

What Are the Long-Term Effects of High Student Debt?

High levels of student debt can have long-lasting consequences that extend far beyond graduation. One major impact is the restriction it places on financial freedom. Graduates burdened with significant debt may find it challenging to pursue their passions, take risks in their careers, or even start families. This can create a cycle of financial stress that lasts for years, affecting not just the individual but also the economy as a whole.

Can High Student Debt Affect Mental Health?

Indeed, the stress associated with high student debt can lead to serious mental health issues. Many graduates experience anxiety and depression tied to their financial situations, which can hinder their ability to thrive professionally and personally. It’s essential for borrowers to recognize the potential psychological impacts of their financial decisions, as these can be just as significant as the monetary costs.

What Are Some Alternatives to Borrowing the Maximum Amount?

Students and families should explore various alternatives before deciding to borrow the maximum amount allowed by federal loans. Some options include:

- Applying for scholarships and grants

- Working part-time during school

- Exploring in-state tuition options

- Considering community college for the first two years

By pursuing these alternatives, students may be able to reduce the amount they need to borrow, ultimately leading to a healthier financial future.

How Can Borrowers Manage Their Student Loans Effectively?

For those who have already borrowed the maximum allowed amounts, effective management of student loans becomes crucial. Strategies for managing student debt include:

- Choosing an appropriate repayment plan

- Making extra payments when possible

- Staying informed about loan forgiveness programs

- Seeking financial literacy resources to understand loan terms

Being proactive about loan management can help mitigate some of the negative effects of high debt levels.

What Should Students Consider Before Borrowing?

Before deciding to borrow the maximum allowed amount of federal loans, students should consider their future earning potential and career path. Understanding the expected salary in their chosen field can provide valuable insights into whether taking on such debt is feasible. Additionally, creating a budget that factors in loan repayment can help students visualize their financial futures and make informed decisions about borrowing.

Conclusion: Why It’s Important to Assess Borrowing Decisions Carefully

Ultimately, students must carefully assess the decision to borrow the maximum allowed amount of federal loans. While it may provide immediate financial relief for educational expenses, the long-term consequences can be severe, affecting both financial stability and emotional well-being. By understanding the risks and exploring alternatives, students can make informed choices that support their educational and financial goals without falling into the trap of overwhelming debt.

You Might Also Like

Understanding The Elasticity Of Demand: What Type Of Good Is This? Group Of Answer ChoicesMonarchs And The Wealth Of Towns: A Historical Perspective

Eutrophication: Understanding Its Causes And Effects

Understanding The Concept Of Noon: What You Need To Know

Exploring A World Of Flavors: Fun And Delight In Every Bite

Article Recommendations