Managing finances is a crucial aspect of life, and understanding how different factors affect our financial decisions is key. One such factor is the relationship between interest payments and the available amount for withdrawals. For many individuals and businesses, interest payments can significantly impact their liquidity, leaving them with less money for withdrawals. In this article, we will explore this intricate relationship, delving into the reasons why interest payments can reduce the funds available for withdrawals and how one can navigate these challenges effectively.

Interest payments are typically associated with loans, mortgages, and other forms of credit. When individuals or businesses borrow money, they are often required to pay interest on the outstanding balance. This payment is an additional cost of borrowing and can accumulate over time, reducing the overall funds available for other financial commitments. As a result, understanding the nuances of interest payments is vital for anyone looking to maintain a healthy financial status.

Furthermore, the implications of these payments can vary based on the type of loan, the interest rate, and the repayment terms. For instance, a higher interest rate can lead to larger payments, which in turn can restrict the amount of money one can withdraw for other expenses. By examining these dynamics, we can gain insight into how to manage our finances better and prioritize our financial goals, ensuring that we maintain both liquidity and the ability to meet our obligations.

What Are Interest Payments?

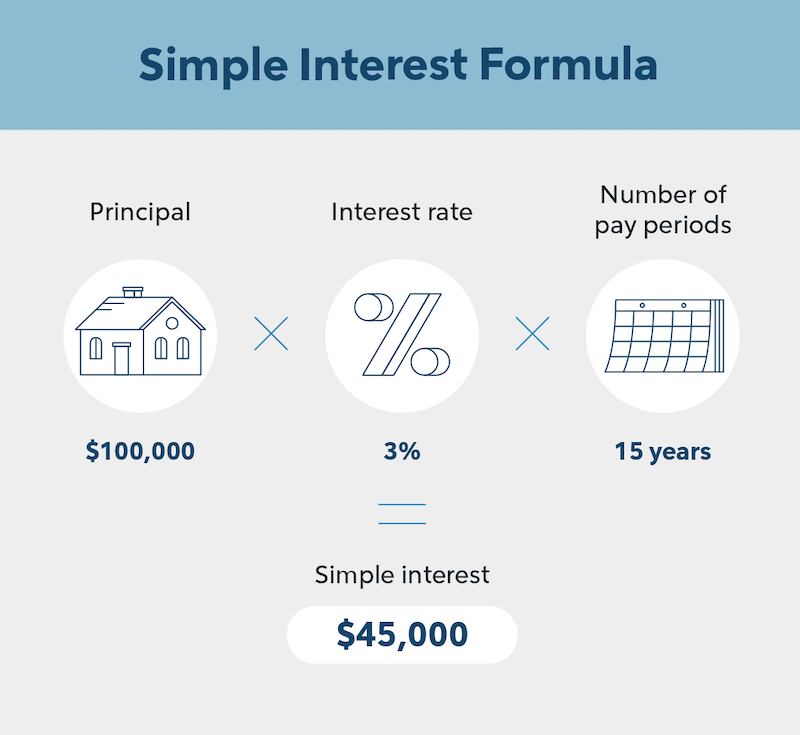

Interest payments refer to the cost incurred by borrowers for utilizing borrowed funds. This cost is expressed as a percentage of the principal amount borrowed and is typically paid periodically (monthly, quarterly, or annually). The key components of interest payments include:

- Principal: The original amount borrowed.

- Interest Rate: The percentage charged on the principal amount.

- Term: The duration over which the loan is to be repaid.

How Do Interest Payments Affect Cash Flow?

Cash flow is the movement of money in and out of a business or individual's finances. Interest payments can significantly affect cash flow in the following ways:

- Reduced Available Funds: As interest payments consume a portion of the available cash, it leaves less money for other expenses.

- Budget Constraints: High interest payments can force individuals or businesses to adjust their budgets, potentially leading to cutbacks in essential areas.

- Opportunity Costs: Money spent on interest payments could have been used for investments or savings, leading to lost opportunities.

Can Interest Payments Lead to Financial Strain?

Yes, excessive interest payments can put significant financial strain on borrowers. This strain can manifest in various ways, including:

- Increased Debt Burden: Higher interest payments can contribute to a cycle of debt, making it challenging to keep up with other financial obligations.

- Stress and Anxiety: Financial stress due to mounting interest payments can affect mental well-being.

- Credit Score Impact: Missing payments or defaulting can lead to a negative impact on credit scores.

How to Manage Interest Payments Effectively?

Managing interest payments is essential for maintaining a healthy financial status. Here are some strategies to consider:

- Refinancing: Consider refinancing high-interest loans to reduce monthly payments.

- Budgeting: Create a budget that accounts for interest payments to ensure timely payments.

- Prioritizing Debt Repayment: Focus on paying off high-interest debts first.

What Are the Alternatives to High-Interest Loans?

There are several alternatives to high-interest loans that individuals and businesses can consider:

- Personal Loans: Look for personal loans with lower interest rates.

- Credit Unions: Consider borrowing from credit unions, which often offer lower rates.

- Peer-to-Peer Lending: Explore peer-to-peer lending platforms for competitive rates.

How Can One Improve Their Credit Score to Access Better Rates?

Improving your credit score can lead to better interest rates and lower payments. Some tips include:

- Pay Bills on Time: Timely payments positively impact your credit score.

- Reduce Credit Utilization: Keep credit card balances low compared to credit limits.

- Regularly Check Your Credit Report: Monitor your credit for errors and dispute inaccuracies.

Conclusion: The Balance Between Interest Payments and Withdrawals

In conclusion, understanding the relationship between interest payments and available funds for withdrawals is crucial for effective financial management. With careful planning, budgeting, and proactive strategies, individuals and businesses can navigate the challenges posed by interest payments, ensuring that they have enough liquidity to meet their financial needs. By making informed financial decisions, one can strike a balance between managing interest obligations and maintaining the necessary funds for withdrawals.

You Might Also Like

The Intricacies Of Spacecraft Fuel Systems: A Comprehensive GuideEmpowering Voices: The Importance Of Exercising Freedom Of Speech As A Space For Civic Engagement

Monarchs And The Wealth Of Towns: A Historical Perspective

Late, Waiting For The New Customers To Give Him Their Orders, Then: A Journey Through Time

If You Are Tired Or Just Cannot Seem To Understand The Material, A Read The

Article Recommendations

:max_bytes(150000):strip_icc()/interest-rates-1d0e17952d9949b1bab273e830855f90.png)

:max_bytes(150000):strip_icc()/interest.asp-final-c3fdffd368294a708ea21ff11cd4df06.png)